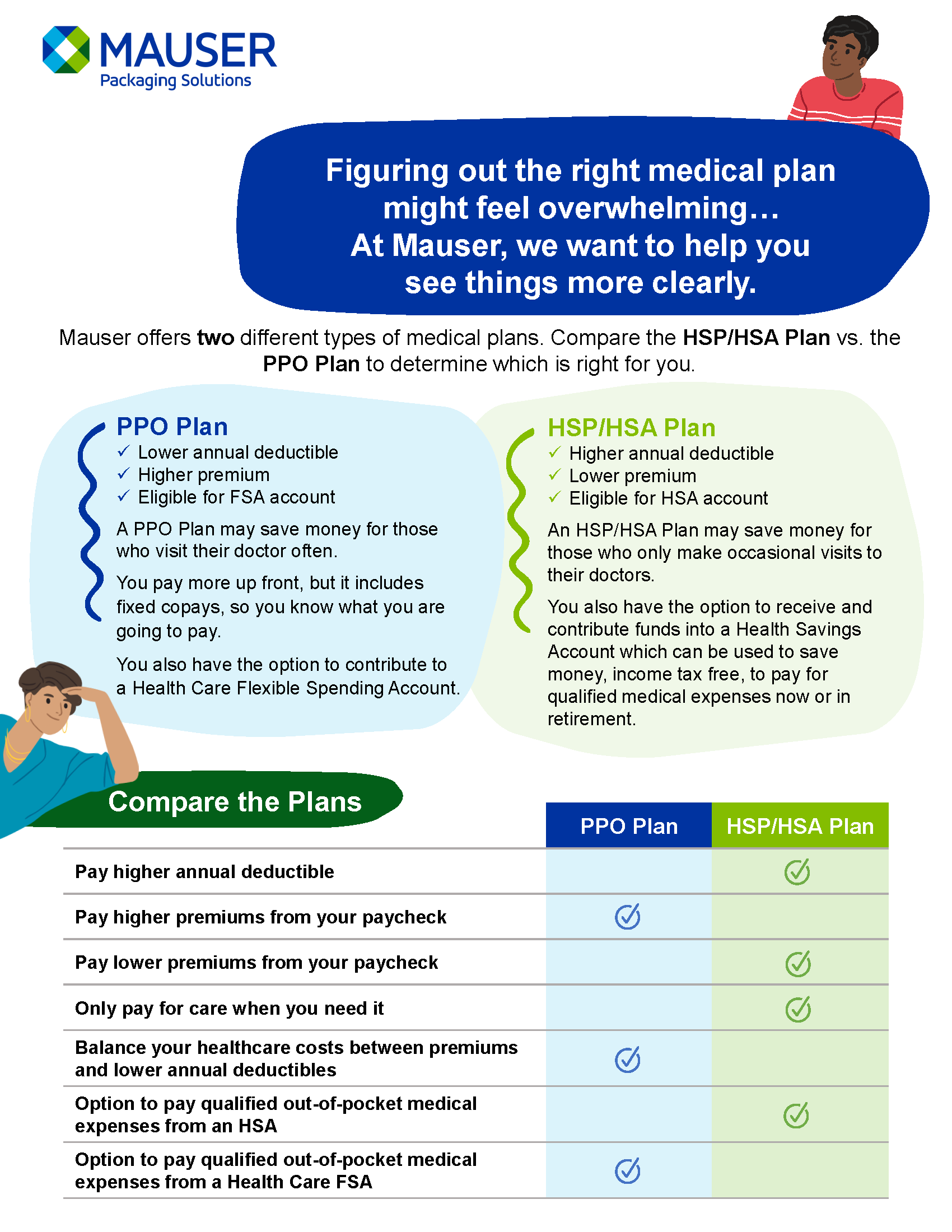

When trying to decide on healthcare benefits, figuring out the right medical plan for you and your family is important. To meet the need of our diverse employee population, Mauser Packaging Solutions currently offers two health plan options: 1) an HSP/HSA that is a high deductible health plan (known as an HDHP) and 2) a preferred provider organization (known as a PPO).

Ahead, we explore differences between HDHPs (high deductible health plans) and traditional PPOs (preferred provider organizations). Mauser’s HDHP and PPO medical plans include access to UnitedHealthcare’s national Choice Plus Network of providers for in-network benefits. Additionally, both plans include 100% coverage for preventative care.

Understanding an HDHP

An HDHP, or high deductible health plan, is a type of health insurance plan that features higher upfront out-of-pocket costs and deductibles, but with lower monthly premiums (from your paycheck) in comparison to a PPO.

HDHPs can be ideal for those who only make occasional visits to a doctor. With higher deductibles and out-of-pocket maximums, the value of an HDHP can start to diminish as visits, procedures, and prescriptions become more frequent.

Mauser’s HSP/HSA Plan is a high deductible health plan with a Health Savings Account (HSA). An HSA can be used to help cover your deductible, prescription medications, or other health care expenses. Funds are not taxed and are deposited into an HSA as part of a payroll deduction.

Understanding a PPO

A PPO, or preferred provider organization, is a health insurance plan that works with a network of providers who offer certain rates for those enrolled in the plan. This plan features lower out-of-pocket costs and deductibles, but with higher monthly premium (from your paycheck) in comparison to an HDHP.

With lower deductibles and out-of-pocket maximums, PPOs can help balance the costs for those who visit their doctors more often and can help lead to savings once all medical expenses are paid.

Those enrolled in a PPO can contribute to a Health Care Flexible Spending Account (FSA). An FSA can be used to help cover your deductible, prescription medications, or other health care expenses within the year. Funds are not taxed and are deducted as part of a payroll deduction.

|

HDHP |

Traditional PPO |

|

|

Monthly premiums |

Lower |

Higher |

|

Deductibles and out-of-pocket maximums |

Higher |

Lower |

|

Pre-tax saving option for out-of-pocket expenses |

Health Savings Account (HSA) |

Health Care Flexible Spending Account (FSA) |

Which plan is right for you?

Choosing the right health insurance plan will vary by individual and depends on lifestyle, anticipated health care needs, and ability to cover out-of-pocket expenses. Compare the monthly premiums and deductibles of both plans and think about the type of healthcare you utilize annually. Regardless of which insurance plan you choose, it’s always a good idea to take advantage of the savings opportunities your health coverage provides. Setting aside some money in an HSA or FSA can help prepare you for medical expenses, whether they result from a high deductible or a traditional PPO.

Example Scenarios:

HDHP with HSA: Managing some health conditions and maintenance medications

Medical Status: Michael is a 52-year-old manager from Georgia. While he’s always prioritized in his family taking part in physical activities, at times this has been difficult for two working parents and their high school aged sons. For the past few years, Michael has been seeing his doctor for on-going high blood pressure and high cholesterol, which seems to run in the family. Like him, his spouse is also managing a high blood pressure diagnosis and low vitamin D.

Financial Risk Factor: Health conditions and maintenance medication can lead to high medical costs.

Which plan do they choose? They choose family coverage in the HSP/HSA plan. Despite the parents’ on-going health conditions, the family doesn’t mind paying the higher upfront fees when seeing their in-network doctors every 3-4 months and filling their medications which are considered low-tier (less costly).

Covering Out-of-Pocket Expenses:A Health Savings Account (HSA) enables him to contribute pre-tax funds to cover the deductible and invests his account in mutual funds to build up savings for future health care needs. Michael chooses to contribute pre-tax funds from his paycheck into the HSA, moreover, his employer also contributes $1,000 a year to his HSA.

PPO: Having flexibility in foreseeable costs

Medical Status: Sofia, 36, of Chicago has been married for five years and works in customer service. She’s been overall healthy and is active in her day-to-day life. However, Sofia is pregnant, and she anticipates having testing and following-up with a gynecologist and expenses for the delivery of the baby.

Financial Risk Factor: Additional tests, evaluations, and/or treatment can lead to high medical costs.

Which plan does she choose? Sofia is young, active, and overall healthy. Every evening she walks around the park with her dog and takes long hikes with her husband on the weekends. Other than preventive care, she typically has minimal health care needs. However, because the couple has a baby on the way, she chooses the PPO plan.

Covering Out-of-Pocket Expenses: Knowing she’ll need more health care in the coming year and that she can afford higher premiums (from her paycheck), a PPO is a good choice. Pairing it with a Health Care Flexible Spending Account (FSA) will allow Sofia to save money by contributing pre-tax funds to cover her copays, deductible, and prescriptions.