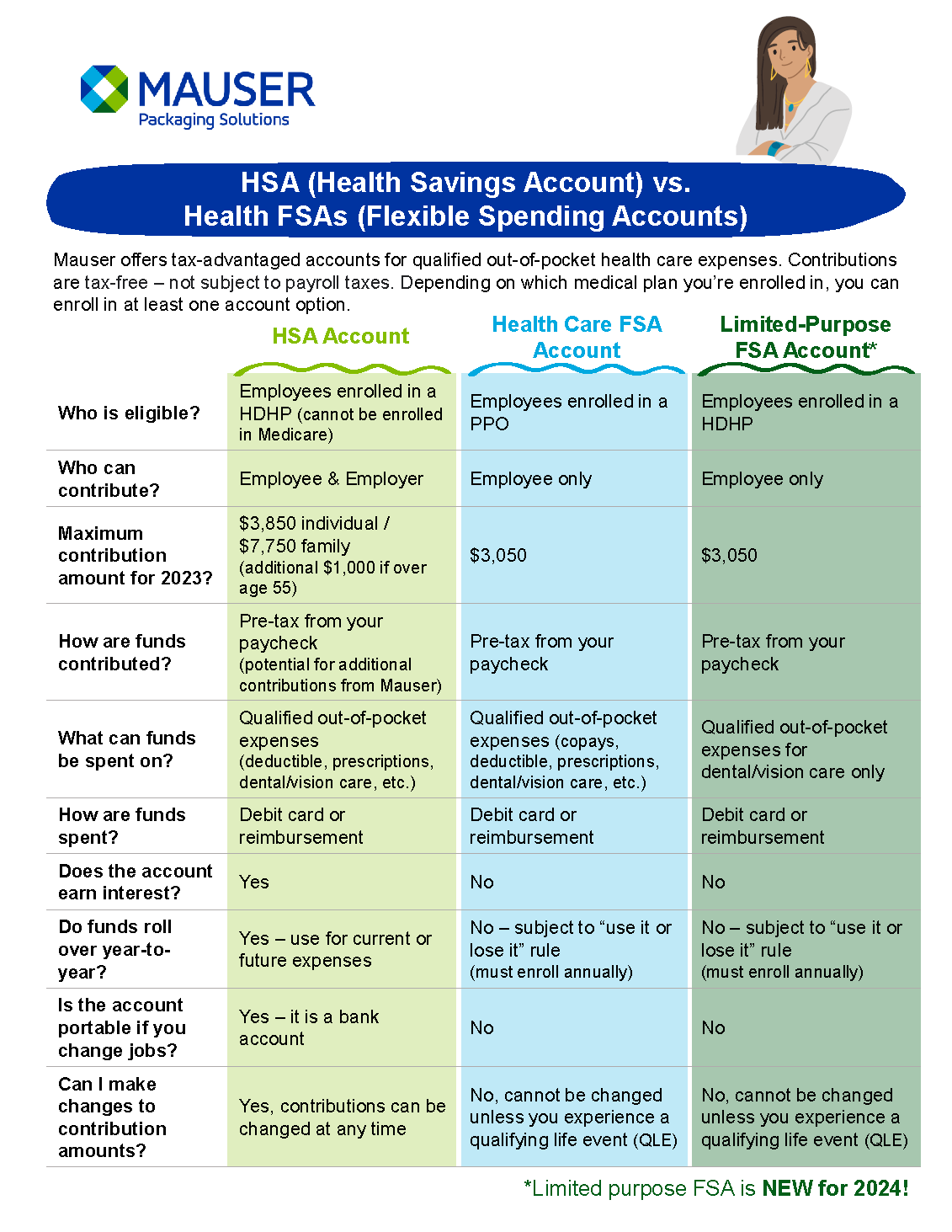

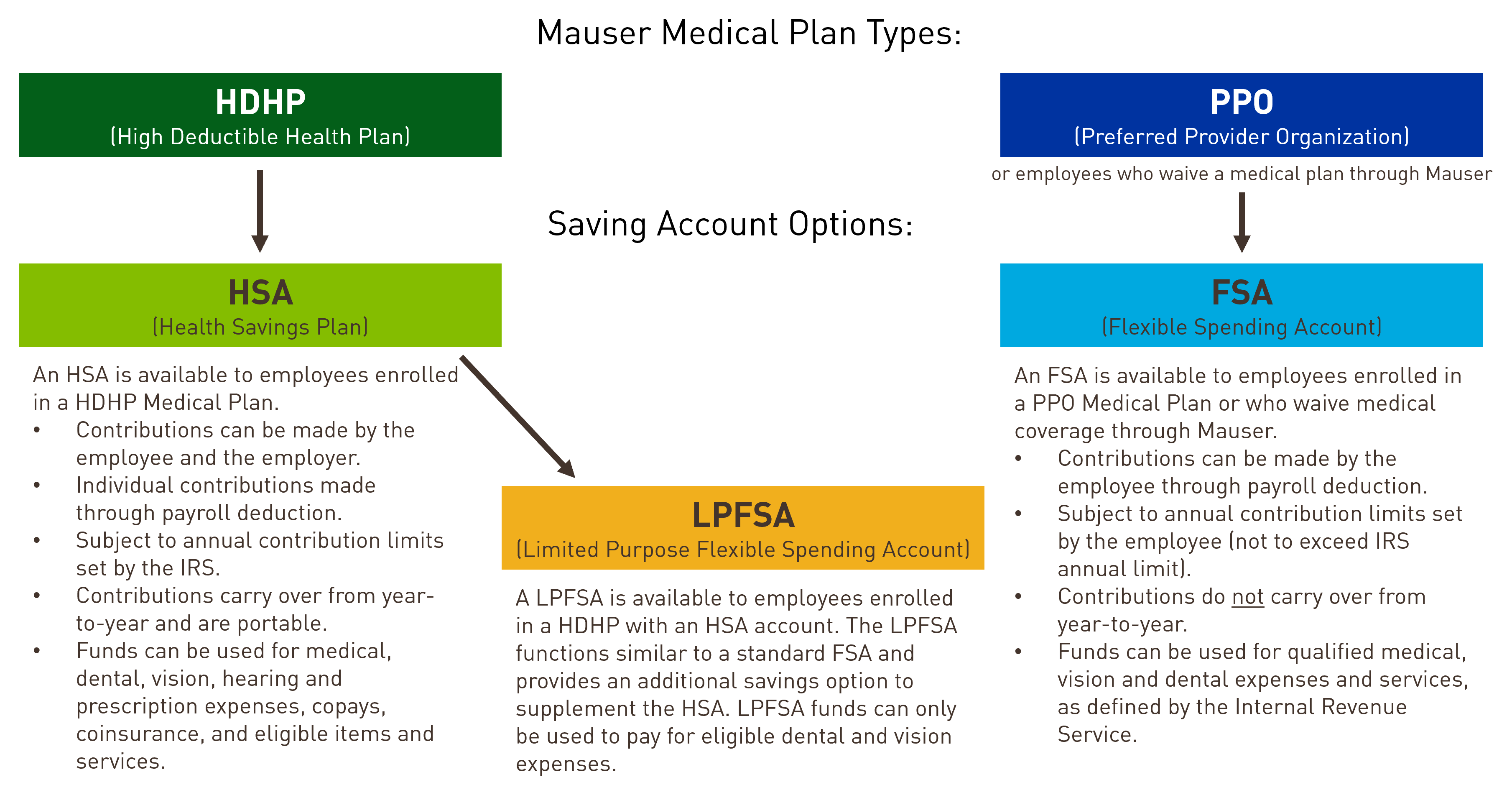

Medical insurance plans can go a long way to cover medical expenses but regardless of plan type, there are always out of pocket expenses associated with deductibles, co-pays, medications, medical supplies and more. Tax Advantaged Savings Accounts help you plan for these expenses through contributions that are tax-free meaning contributions are not subject to payroll taxes (i.e., you don’t have to pay federal, state or Social Security taxes on this money). Depending on which medical plan you’re enrolled in, you may have access to a Health Care Flexible Spending Account (FSA), Health Savings Account (HSA) and/or a Limited-Purpose FSA Account (LPFSA).

Let’s dive a little deeper into what FSAs, HSAs and LPFSAs are, how they work, and what you can use the funds for. Don’t miss out on your benefits – knowing these differences may help you know how to use these accounts to your advantage.

Health Care Flexible Spending Account (FSA)

What is a Health Care FSA?

A Health Care Flexible Spending Account (FSA) is designed to help employees set aside money to pay for out-of-pocket health care costs during the plan year. Contributions to an FSA provide a tax break since they are not subject to payroll tax.

Eligibility:

Only employees enrolled in the PPO medical plan or who waive medical coverage through Mauser are eligible to enroll in the Health Care FSA plan.

How do FSA's work?

- Employers set the maximum amount that you can contribute; however, it can’t exceed the annual IRS limit. Mauser’s FSA limit for 2024 is $3,050. Limits have not been set for 2025.

- An FSA is not a savings account. If you leave your job, you can’t take your FSA with you.

- If you don’t use the full amount you’ve elected to contribute by the end of the calendar year, you could lose, or forfeit, your FSA dollars.

- You must enroll annually during Open Enrollment, so you’ll have to decide how much money you want to set aside for the year.

- Using your FSA is easy. Your FSA comes with a handy debit card, which makes it easy to pay for services from your FSA. Other options include:

- Automatic payment-Claims from UHC Medical and Rx will automatically rollover and reimburse you from the FSA.

- Online claim form-Easily submit claims on myuhc.com to get reimbursed from your FSA.

- Direct deposit-UHC can reimburse your money directly into your personal bank account.

How can I use the money in my health care FSA? What can I buy?

You can use your FSA for qualified medical expenses and services, as defined by the Internal Revenue Service. What The list of qualified medical expenses is extensive, but some of the more common expenses and services include:

- Deductibles

- Copayments

- Prescription medication

- Over-the-counter medication

- Vision care, including prescription eyeglasses and contact lenses

- Thermometers

- First-aid kits

- Hearing aids

- Diabetic supplies

- Chiropractic care

Resources

- Click here for more information on FSAs.

- Not sure how much to put in your FSA? Click here to use UHC’s FSA Savings Calculator.

- Click here for more information on HSAs; see page 6 for Eligibility Information.

- Not sure how much to put in your HSA? Click here to use Optum’s HSA Savings Calculators.

- For a complete list of eligible expenses, click here to review Internal Revenue Service (IRS) Publication 502.